UPDATE effective April 1, 2018: The North Carolina Reinsurance Facility surcharge is increasing again from 11.45% to 13.24% due to higher sustained losses in the Reinsurance Facility. Per state law, the surcharge is combined with BI/PD premiums and charged to all policyholders with all companies across the state.

————————————————

“Why have my insurance bills gone up?”

It’s one of the most common questions we get asked when clients receive their renewal offers and see that their premiums have risen despite not having made any changes to their coverage. This can be due to any number of reasons – the easiest of which to comprehend are claims for accidents, or speeding tickets that may have been acquired during the previous year.

However, a common culprit for premium increases that most people don’t know about is something called a “recoupment charge,” which may appear on your policy labeled as “NCRF Clean Risk Allocation.” It can sound complicated but we’ll explain it to you as best we can.

As you probably know, North Carolina requires every driver to carry liability insurance, no matter how high of a risk they may be to insure. Because everyone needs coverage by law, insurance companies are not permitted to turn away high risk drivers who are seeking the required coverage. To prevent any one company from taking on too much risk, in 1973 the North Carolina Reinsurance Facility (NCRF) was created to ensure that all eligible drivers are able to purchase a policy.

The goal of the NCRF is to distribute losses proportionally across all member companies to offset the high-risk policies that some companies may take on. Insurance companies may pass, or cede, certain high risk policies to the NCRF to avoid the potential losses. The amount of state drivers covered by the NCRF can hover around 25 percent, and when many of those drivers prove to be the risks they were thought to be, the NCRF loses money. Because the NCRF typically operates at a deficit each year, the “recoupment charge” was created by the North Carolina Rate Bureau (NCRB) to help balance this out. This charge is added to all North Carolina auto policies with all companies. It increased from 4 percent to 9 percent in October 2016, and was again increased to 11 percent on April 1, 2017.

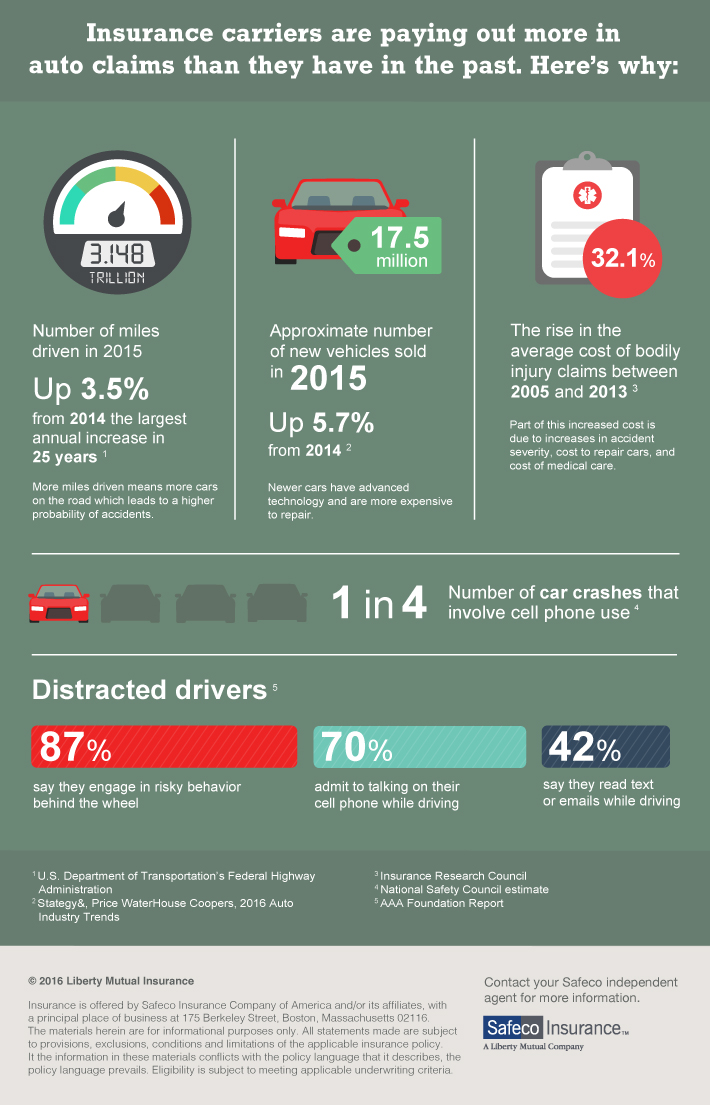

How is this rate calculated? Again, there a number of factors. One of the main reasons is inflation. The cost to repair vehicles damaged in accidents has increased dramatically, while medical costs have risen for accident injury victims. The population continues to grow in North Carolina, and with more people comes more accidents and claims.

Here are some facts from the NCRB:

-In 2015, the most recent year available, fatalities increased 8.1 percent from 2014, injuries increased 11.8 percent and reported crashes were up 11.1 percent.

-Mileage driven in 2015 was up 13 percent from the average of the preceding five years.

-Inflation in 2016 has increased vehicle repair costs by 2.4 percent and total medical care costs by 3.8 percent.

-The NCDMV estimates that there were 7 percent more crashes in 2015 due to distracted driving and 13.2 percent more alcohol related crashes.

All of these factors are considered when there is a rate increase, and clients will start to see those rate increases reflected in the premiums as renewal dates come around.

Here at Brown-Phillips, we’ll certainly do anything we can to help you offset these increases by finding other ways to reduce your premium. Are you interested in reducing your coverage or raising your deductible? Are you able to pay your premium in full as opposed to installments? Would you like to bundle the policy with a homeowner’s or renter’s policy? Sometimes these things can enact discounts that could help counteract the rising costs.

On the bright side, it’s also key to note that in spite of these changes, North Carolina drivers still enjoy the fourth-lowest auto insurance rates in the entire country. Thanks again for the chance to review and service your insurance needs.